For Busy Reader

Trump and Nixon resemble each other in obvious ways. Both projected strong presidential power, distrusted the press and bureaucracy, and tended to see alliances less as communities of trust than as arrangements that needed a clearer bill. For investors, though, temperament is the smaller story. The larger question is whether political discretion can collide with tariffs, inflation, rates, deficits, and dollar trust at the same time.

The 1970s bear market was not created by Watergate alone. By the time the scandal broke into the center of American politics, the economy was already being hit by the 1971 suspension of dollar-gold convertibility, a 10% import surcharge, the 1973 oil shock, high inflation, higher rates, and recession. Watergate became a crisis of trust layered on top of a weakening economic order. The Trump-era question should be framed the same way: not “will there be another Watergate,” but whether politics is making the basic economic rules harder to trust.

Today is not the 1970s. The dollar is no longer tied to gold, the US economy is much more exposed to technology, software, and AI investment, and the Federal Reserve has a deeper inflation-fighting playbook. A literal replay is unlikely. But a tariff shock that keeps prices sticky, prevents the Fed from easing, lifts long-term rates through deficits, and raises corporate costs through alliance and supply-chain stress would still be a difficult regime for equities.

The takeaway is simple. What returns is not the person. It is the set of conditions markets dislike. When unpredictable political power presses on prices, rates, the dollar, fiscal credibility, and alliances at once, politics stops being background noise.

The Similarity Is Structural Before It Is Personal

Nixon took office when the United States was carrying the costs of Vietnam, Cold War commitments, inflation, and a weakening dollar promise. The postwar system had been built around American credibility. By the late 1960s, that credibility was expensive to maintain. Dollars had accumulated abroad, gold reserves were finite, and foreign governments had reason to ask whether the United States could keep the dollar-gold link intact.

The Trump-era fatigue looks different, but it comes from a related place. China has become the central strategic rival. Inside the United States, resentment over manufacturing loss and trade deficits has been building for decades. Defense burden-sharing, immigration, fiscal deficits, and high rates all sit inside the same political mood. “America First” is not only a slogan. It is also a sign that many voters no longer want the United States to pay the old price of the old order.

That is why the parallel starts with imperial fatigue, not personality. Nixon and Trump both promised to restore American strength. Yet the promise also revealed strain: the existing order could no longer be carried in the old way without domestic resistance.

Strong Presidents Are Not the Same as Predictable Power

Markets do not automatically dislike strong governments. Tax cuts, deregulation, and industrial policy can be market-friendly if the direction is clear. The problem is not strength. The problem is unpredictability. When companies cannot tell whether today’s tariff is a bargaining chip, a long-term rule, or a domestic political signal, they delay investment. Delayed investment eventually shows up in employment, earnings, and confidence.

Nixon distrusted the press, the antiwar movement, Democrats, and the bureaucracy. Power narrowed into the White House, and Watergate exposed the danger of that closed circle. What began with the 1972 break-in at the Democratic National Committee offices became an obstruction scandal, a congressional investigation, and an impeachment crisis. Nixon resigned on August 9, 1974.

Trump also prefers personal loyalty over institutional distance, direct orders over bureaucratic mediation, and direct communication with supporters over traditional media filters. Supporters may read this as forceful leadership. Markets read another possibility: policy can turn with the president’s negotiating style and political calendar. Ipsos’s Reuters/Ipsos polling showed Trump’s approval at 34% in late April 2026. Still, weak public approval does not mean a Nixon-style collapse inside the party. Trump’s core coalition may hold longer, and that can turn political stress into a more extended period of institutional conflict rather than a quick break.

Alliances: Community of Values or Invoice?

Nixon wanted the United States to stop carrying every war and every defense burden directly. The Nixon Doctrine did not abandon allies, but it asked them to take more responsibility for their own defense. It was a strategic retreat shaped by Vietnam fatigue, Cold War costs, and domestic pressure.

Trump also sees alliances through cost. When he talks about NATO, Korea, Japan, the European Union, or Canada, the first question is often not historic trust but who pays, how much, and what the United States gets in return. Voters may find that direct. Corporations find it harder. Alliances are not only military relationships. They are supply chains, currency arrangements, energy security, and long-term investment environments.

There is an important difference. Nixon’s diplomacy was transactional, but it was also highly strategic. The opening to China, détente with the Soviet Union, and the exit from Vietnam used the Cold War triangle carefully. Trump’s diplomacy is more public, more immediate, and more openly coercive. Nixon tried to rebalance alliance burdens. Trump tries to reprice them.

The Economic Core Was Nixon Shock, Not Watergate

To understand a 1970s-style slump, start with the Nixon shock, not the scandal. In August 1971, Nixon suspended the dollar’s convertibility into gold, froze wages and prices, and imposed a 10% import surcharge. The U.S. Office of the Historian describes this as the beginning of the end of the Bretton Woods fixed-exchange-rate system. The dollar-gold link, US monetary credibility, and the postwar trade order all moved at once.

Trump’s key tool is the tariff. In February 2025, the White House announced 25% additional tariffs on imports from Canada and Mexico, 10% additional tariffs on Chinese imports, and a lower 10% rate on Canadian energy resources. For Trump, tariffs are not merely taxes on imported goods. They are tools for China policy, manufacturing politics, allied pressure, immigration leverage, security bargaining, and fiscal rhetoric.

The macro issue is that tariffs touch prices and investment decisions. They raise import prices, lift corporate costs, and force supply-chain adjustments. Tariffs do not always become broad inflation immediately. Exchange rates, margins, weaker demand, and alternative suppliers can absorb part of the hit. But when inflation is already uncomfortable and rates are not low, a new tariff shock becomes harder for markets to shrug off.

Markets Fear a Broken Economic Order More Than Scandal

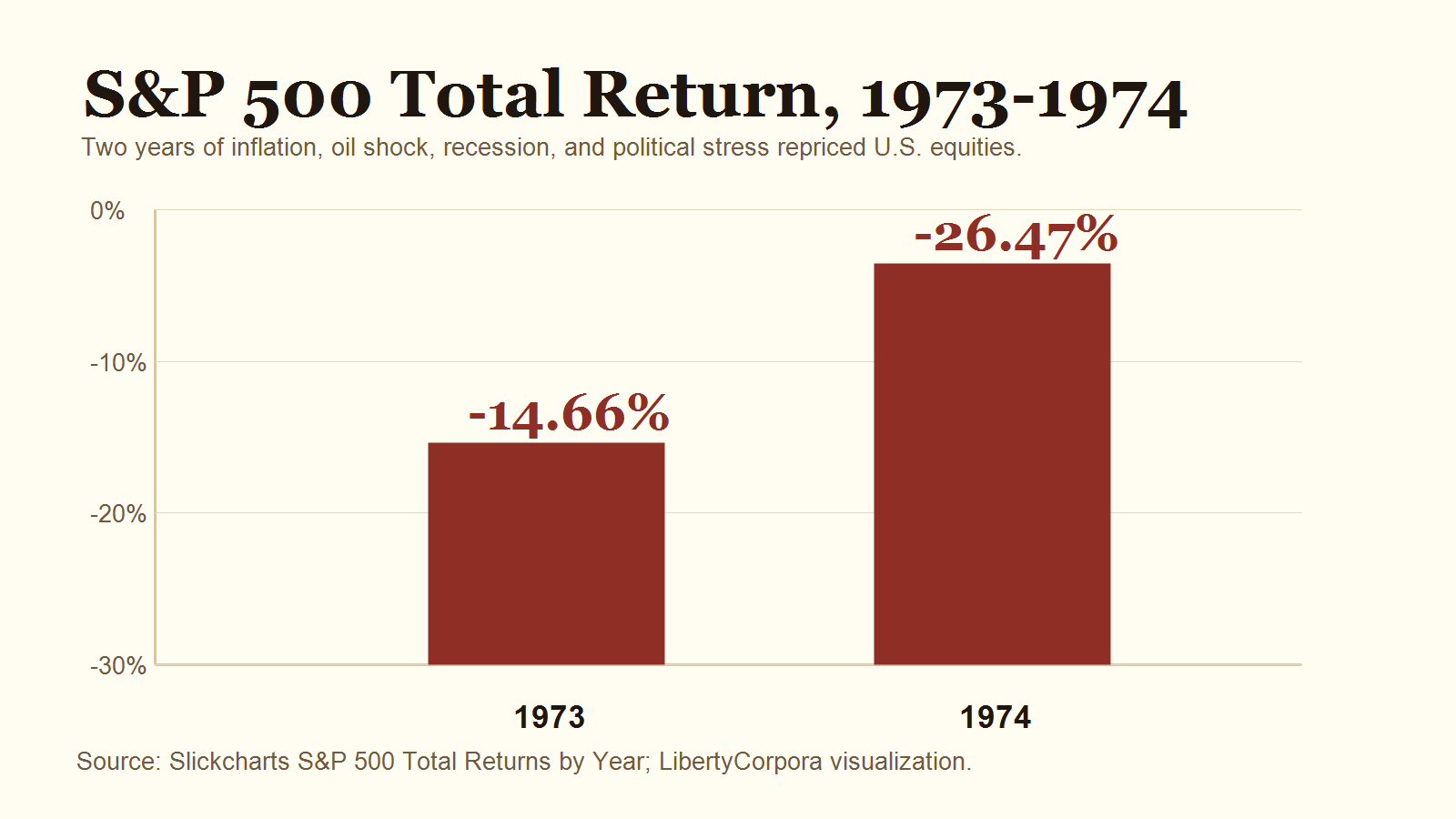

The 1973-1974 equity decline cannot be reduced to Watergate. The S&P 500’s total return was -14.66% in 1973 and -26.47% in 1974, but the deeper backdrop was inflation, the oil shock, the changing dollar system, higher rates, and recession. By NBER dates, the US recession ran from November 1973 to March 1975.

Markets dislike political scandal, but scandal alone rarely creates a long market regime. What markets fear is politics breaking the rules by which costs, rates, money, and policy credibility are priced. When companies cannot forecast costs, investors cannot trust the rate path, central-bank independence is questioned, and the dollar or Treasury market feels less secure, politics becomes macro.

That question remains live in 2026. BLS reported April 2026 CPI up 3.8% year over year, with core CPI up 2.8%, and energy prices contributing heavily. At its April 2026 meeting, the Federal Reserve held the federal funds target range at 3.5-3.75%. This is not the runaway inflation of the 1970s. But it does mean tariffs and energy shocks could make it harder for the Fed to pivot quickly toward easier policy.

Fiscal policy adds another pressure point. CBO projects the US deficit at 5.8% of GDP in 2026 and 6.7% in 2036. Federal debt held by the public is projected to rise from 101% of GDP in 2026 to 120% in 2036. That path can keep a floor under long-term rates. Higher long-term rates are especially uncomfortable for growth stocks whose value depends on profits far in the future.

This Is Not the 1970s

A simple replay is the wrong base case. First, the world is not on gold. Nixon broke a dollar-gold promise. Today’s dollar already floats inside a fiat-money system. A new Nixon shock would more likely appear through Treasury-market confidence, central-bank independence, dollar demand, or tariff order, not through a gold window.

Second, the US economy is different. The 1970s economy was more directly exposed to manufacturing and energy shocks. Today, large technology platforms, software, and AI investment are central pillars of market earnings. Even if a 1970s-like pressure cycle appears, sector dispersion is likely to matter more than a simple across-the-board collapse.

Third, the political structure is different. Nixon lost public support and then lost his party’s protective wall. Trump can face weak approval while keeping a more durable core coalition. That means stress may not end in a single dramatic resignation-style event. It may instead stretch into a longer fight over institutions, policy, and credibility.

Conclusion: Conditions Repeat More Often Than People

The memory of Nixon is usually filed under Watergate. For investors, that is too narrow. The more useful lesson is what happens when political distrust lands on top of an already unstable economic order.

The real Trump-era question is not whether there will be a second Watergate. It is whether tariffs keep inflation sticky, inflation keeps the Fed from easing, deficits lift long rates, alliance distrust raises corporate costs, political conflict weakens confidence in institutions, and equity valuations lose their old ceiling.

If those conditions build together, a few 1970s-style features can return: weaker tolerance for expensive growth stocks, pressure on rate-sensitive assets, greater demand for cash flow, and more interest in real assets, energy, defense, staples, and dividends. That does not mean the same crash must happen. It means the market’s preferred regime can change.

If tariffs cool, inflation settles, rates fall, and corporate earnings hold, the Nixon analogy will look exaggerated. History does not return wearing the same face. But the conditions markets fear do repeat. When politics shakes the economic order, markets stop treating politics as only politics.

Sources

- U.S. Office of the Historian, Nixon and the End of the Bretton Woods System

- Federal Reserve History, The Great Inflation and Oil Shock of 1973-74

- NBER, US Business Cycle Expansions and Contractions

- The White House, Fact Sheet on Canada, Mexico and China tariffs

- BLS, Consumer Price Index Summary, April 2026

- Federal Reserve, FOMC statement, April 29, 2026

- CBO, The Budget and Economic Outlook: 2026 to 2036

- Ipsos, Latest U.S. opinion polls

- Slickcharts, S&P 500 Total Returns by Year