For busy readers

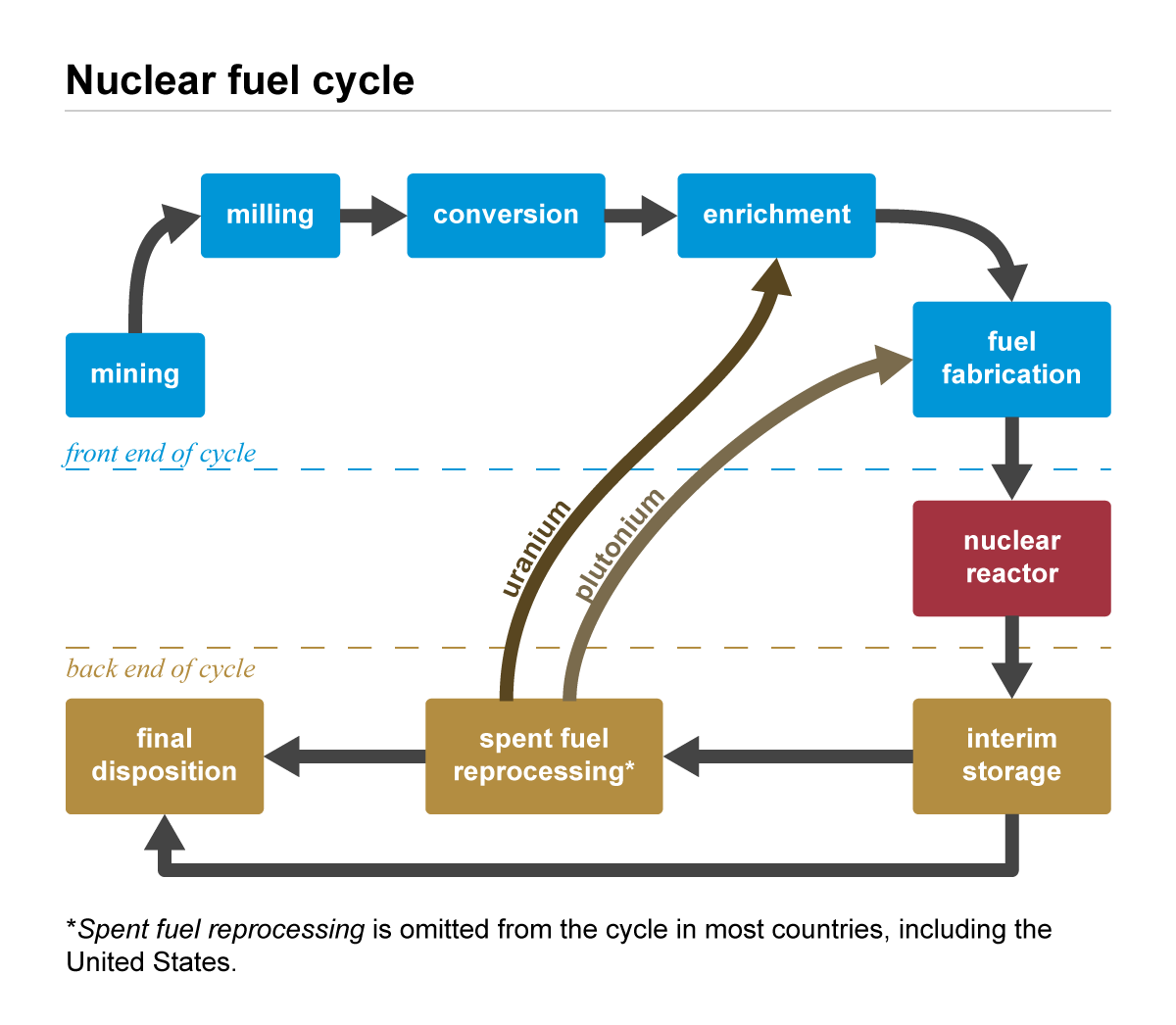

The uranium thesis is not simply “more nuclear plants, therefore higher uranium.” That is the easy version. The more useful version starts with the nuclear fuel cycle: mining, milling, conversion, enrichment, fuel fabrication, reactor operation, and spent-fuel management.

As of May 14, 2026, uranium sits at the intersection of electricity demand, energy security, fuel-cycle bottlenecks, and financial-market access. The direction of nuclear demand looks more supportive than it did a decade ago. The harder question is whether the investable vehicle actually owns the part of the chain where scarcity appears.

That distinction matters. U3O8, uranium miners, nuclear value-chain ETFs, enrichment-linked companies, HALEU suppliers, and nuclear utilities are not the same exposure. They may all belong to the uranium story, but they do not carry the same risk.

Start with the asset, not the ticker

Uranium is a fuel-cycle asset before it is a financial asset. Natural uranium is mined, milled into U3O8, converted into UF6, enriched so the share of U-235 is higher, fabricated into fuel, and then loaded into a reactor. The EIA explains that conventional reactor fuel is typically enriched to 3% to 5% U-235 before it becomes pellets, rods, and assemblies.

This is why uranium is different from oil or copper. A barrel of oil can be refined and burned through a large commercial chain. A pound of uranium concentrate cannot simply move from a warehouse into a reactor. Each stage is regulated, specialized, and politically sensitive.

So the first serious question is not “is uranium scarce?” It is where scarcity appears. Is the constraint in mined U3O8, conversion, enrichment, HALEU, logistics, inventories, or financial vehicles? A correct uranium thesis can still produce a poor result if the investment instrument is pointed at the wrong bottleneck.

Demand is becoming more strategic

The demand story has two layers. The first is conventional nuclear power: life extensions, restarts, higher capacity factors, and new reactors. The second is the broader electricity problem. AI data centres, cloud infrastructure, industrial electrification, and reshoring all need reliable power.

The IEA’s Energy and AI work is useful because it does not treat data centres as a slogan. It estimates that data centres rise from roughly 1% of global electricity generation today to 3% in 2030 in its base case. In the United States, nuclear already supplies about one-fifth of data-centre electricity, and the IEA expects nuclear to matter more after 2030 if SMRs are commissioned.

That does not mean uranium demand explodes tomorrow. Nuclear projects move slowly. Permitting, financing, construction costs, grid interconnection, and public acceptance all decide when demand becomes fuel orders. But the direction is clearer: nuclear power is being revalued as a source of reliable, low-emissions electricity and as an energy-security tool.

The World Nuclear Association’s 2025 fuel report release frames the scale. It estimates global reactor uranium requirements of about 68,920 tU in 2025, rising to just over 150,000 tU in 2040 in the reference scenario. The range matters as much as the central number: the lower case still grows, while the upper case implies a much tighter fuel market.

The bottleneck is wider than the mine

Uranium mining is slow to respond. New mines need exploration, permitting, capital, environmental review, processing infrastructure, and long-term offtake confidence. Higher prices help, but they do not instantly create pounds.

The more interesting constraint is what happens after mining. The EIA’s fuel-cycle description shows why conversion and enrichment are not side issues. Yellowcake has to become UF6, and UF6 has to be enriched before fuel fabrication. If conversion or enrichment is constrained, mined uranium alone does not solve the fuel problem.

HALEU adds another layer. The NRC defines HALEU as uranium enriched so that U-235 is between 5% and 20% of the uranium mass. Many advanced reactor designs propose to use HALEU because higher enrichment can support smaller cores, longer operating cycles, and different reactor designs.

That makes HALEU a strategic bottleneck, not just a niche fuel. If advanced reactors move from demonstration to deployment, the fuel question becomes part of the deployment question. The reactor is not commercial if the fuel supply chain is not ready.

| Stage | Main constraint | Investment meaning |

|---|---|---|

| U3O8 mining | Geology, permits, project timing | Most direct link to spot uranium, but exposed to mining execution risk. |

| Conversion | Industrial capacity and qualification | A midstream bottleneck can matter even when mine supply improves. |

| Enrichment | Centrifuge capacity, regulation, national security | Policy support and long contracts can matter more than the U3O8 spot price. |

| HALEU | Limited commercial supply chain | Advanced-reactor optimism depends on fuel availability, not only reactor design. |

The new-cold-war premium is real, but messy

Uranium now belongs to the same policy family as semiconductors, rare earths, batteries, LNG, and defence supply chains. The point is no longer only lowest cost. It is whether the supply chain can be trusted in a crisis.

The U.S. ban on Russian low-enriched uranium shows the trade-off clearly. The DOE says the ban went into effect on August 11, 2024. Its domestic LEU supply-chain page states that the United States imports 20% to 25% of its enriched uranium from Russia and that the ban runs from August 2024 through December 31, 2040. The same page notes planned DOE funding of $2.7 billion for LEU and HALEU infrastructure capabilities.

That is bullish for fuel-cycle rebuilding, but it is not clean or frictionless. The waiver process exists because nuclear plants still need fuel. A policy can be strategically right and operationally difficult at the same time.

| Policy item | What changed | Why it matters |

|---|---|---|

| Russian LEU ban | U.S. import ban effective August 2024 | Western utilities need alternatives, but fuel continuity still matters. |

| Waiver process | DOE can allow imports under defined conditions | The transition is strategic, not instantaneous. |

| Domestic enrichment support | DOE plans LEU and HALEU infrastructure funding | Fuel services may gain policy support separate from the uranium spot price. |

Separate civilian demand from military demand

For investors, the direct demand to follow is still civilian nuclear power. Utility procurement, long-term fuel contracts, life extensions, restarts, and new reactors sit closest to uranium prices and fuel-cycle company earnings.

Military demand is different. Nuclear weapons, nuclear-powered submarines, and military reactors are connected to enrichment capability, but they do not set the commercial uranium price in the same direct way.

The military angle is better understood as a strategic premium. It supports inventories, domestic capacity, national-security budgets, and fuel-cycle cooperation among allies.

The instrument is half the thesis

Uranium is a market. Uranium exposure is a product choice. The gap between those two sentences is where many investment mistakes happen.

| Vehicle | Core exposure | Main risk |

|---|---|---|

| Physical uranium trust | Closer to U3O8 ownership | NAV premium or discount, liquidity, trust structure, fees. |

| Uranium miners ETF | Mining and development equities | Equity risk, permitting, cost inflation, dilution, country risk. |

| Nuclear value-chain ETF | Miners, utilities, equipment, fuel services | Broader theme exposure can drift away from U3O8 price moves. |

| Enrichment or HALEU company | Fuel-cycle bottleneck and policy contracts | Project execution, budget timing, technology qualification, single-company risk. |

| Nuclear utility | Power generation and regulated electricity economics | Power prices, regulation, rate cases, outages, political risk. |

A physical uranium vehicle can track U3O8 more closely than miners, but it can trade at a premium or discount to its net asset value. A mining ETF can rise more sharply in a uranium bull market, but it also carries mining costs, equity-market beta, and financing risk. An enrichment-linked company may be closer to the strategic bottleneck, yet its outcome can depend more on government contracts than on spot uranium.

That is the practical conclusion: the asset thesis starts with scarcity; the investment result depends on the vehicle.

What can break the thesis

The strongest uranium argument is also vulnerable to timing. Nuclear demand is structural, but reactors are slow. A delayed construction cycle can postpone fuel demand even if the long-term thesis remains intact.

Supply can also respond. Restarts, brownfield expansions, new mines, and long-term contracting can bring material back if prices stay high enough. The response may be slow, but it is not zero.

Policy is the third risk. The same government support that can help enrichment and HALEU can also create uncertainty. Waivers, sanctions, budget delays, safety rules, export controls, and public opposition can all change the path.

Finally, financial vehicles can disconnect from the underlying. Uranium equities can sell off with risk assets. Physical trusts can move around NAV. Thematic ETFs can be dominated by companies that are not pure uranium exposure.

What to watch

The useful checklist is short:

- U3O8 spot and long-term contract prices

- Conversion and enrichment capacity additions

- Russian LEU ban waivers and expiry dates

- HALEU production milestones

- Reactor life extensions, restarts, and new-build approvals

- Data-centre power demand and SMR contracting

- NAV premiums or discounts in physical uranium vehicles

- Valuations and financing conditions for miners and fuel-cycle companies

These signals should be read together. A higher uranium price does not automatically make every uranium stock attractive. A stronger nuclear policy does not automatically make a utility a uranium trade. The whole point is to keep the fuel cycle and the financial instrument separate.

Sources

- World Nuclear Association, World Nuclear Fuel Report 2025 release

- International Energy Agency, Energy and AI: energy supply for AI

- U.S. Energy Information Administration, The nuclear fuel cycle

- U.S. Energy Information Administration, 2024 Uranium Marketing Annual Report

- U.S. Department of Energy, Russian Uranium Ban Waiver Guidance

- U.S. Department of Energy, Domestic Low Enriched Uranium Supply Chain

- U.S. Nuclear Regulatory Commission, High-Assay Low-Enriched Uranium