For Busy Readers

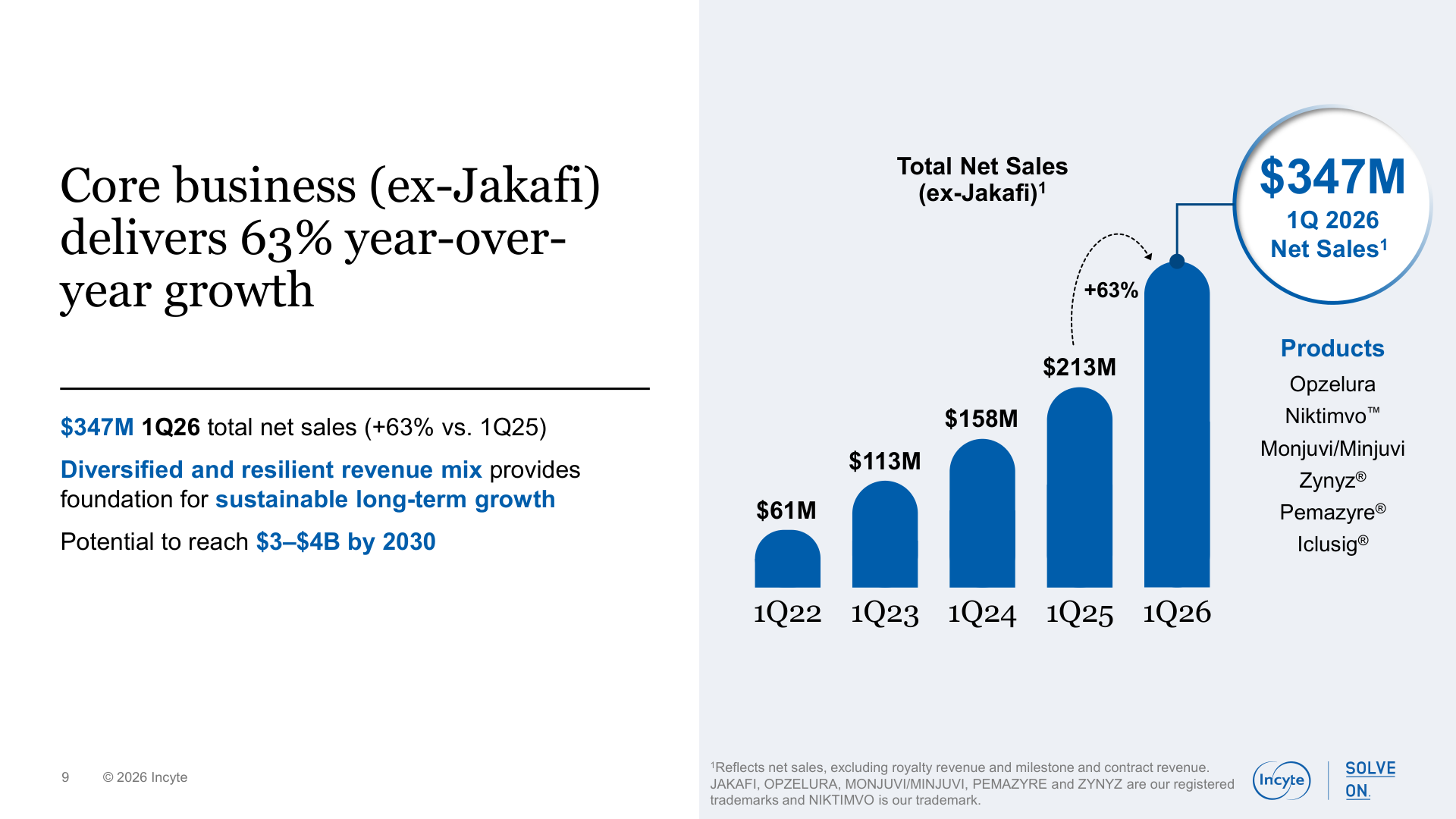

Incyte is not an early-stage biotech story. It already earns money, generates cash, and carries more than enough liquidity to fund late-stage trials. The March 2026 quarter shows that clearly: total revenue was $1.27 billion, operating income was $301 million, and operating cash flow was $369 million.

JAKAFI's strength is also Incyte's largest future risk. JAKAFI still produced $758 million of net sales in the quarter, roughly two-thirds of product sales. But the company says ruxolitinib patent protection, including applicable extensions, expires in mid and late 2028. That does not make Incyte weak today. It means the company has to prepare before the strongest asset starts to lose exclusivity.

The core question is straightforward: is Incyte relying too heavily on JAKAFI, or is it already preparing the next franchise? The evidence points to a company in transition. OPZELURA, NIKTIMVO, ZYNYZ, royalties, and the mutCALR pipeline are real assets. They are not yet large enough to make the transition fully proven.

What Incyte Sells

Incyte develops and sells specialty medicines across hematology, oncology, and inflammation and autoimmunity. In plain language, it sells high-value drugs into specialist markets and receives royalties from partners for some products outside its own commercial footprint.

JAKAFI has been the current center of that business model. In the United States, Incyte sells ruxolitinib as JAKAFI for myelofibrosis, polycythemia vera, and acute or chronic graft-versus-host disease (GVHD). Outside the United States, Novartis sells ruxolitinib as JAKAVI, and Incyte receives royalties.

The next layer is OPZELURA, a topical ruxolitinib cream for atopic dermatitis and nonsegmental vitiligo. FDA describes OPZELURA as the first FDA-approved pharmacologic treatment to address repigmentation in vitiligo patients. That matters because it is not just another dermatology product; it opened a category where approved treatment options were limited.

Then come smaller but fast-growing products: NIKTIMVO in chronic GVHD, ZYNYZ in oncology, and MONJUVI/MINJUVI. These are not yet big enough to replace JAKAFI, but they show whether Incyte can extend its commercial presence beyond one flagship drug.

| Revenue line | Q1 2026 | Why it matters |

|---|---|---|

| JAKAFI | $757.8M | The cash engine. Strong demand, but patent expiry is the central risk. |

| OPZELURA | $143.0M | The most important commercial product for reducing the post-JAKAFI revenue gap. |

| NIKTIMVO | $55.1M | A newer GVHD asset that deepens Incyte's specialist franchise. |

| ZYNYZ | $41.4M | Still small, but part of the non-JAKAFI oncology growth base. |

| Product royalties | $151.2M | High-quality partner revenue from JAKAVI, OLUMIANT, TABRECTA, and other products. |

Why The Post-JAKAFI Plan Matters

There are clear reasons why JAKAFI has been hard to dislodge. In rare blood diseases, prescription habits do not change just because a new drug appears. Doctors care about response, dose adjustment, blood counts, infection risk, reimbursement, and long-running clinical familiarity. JAKAFI has years of that embedded experience.

The GVHD franchise adds to the point. FDA approved ruxolitinib for chronic GVHD in 2021 after REACH-3 showed a 70% overall response rate through Cycle 7 Day 1 versus 57% for best available therapy. That does not make JAKAFI untouchable, but it helps explain why specialist confidence does not change overnight.

Still, this is not a permanent monopoly. The FY2025 Form 10-K says JAKAFI product sales are expected to contribute a significant percentage of total revenue over the next several years, but also says sales are expected to begin declining after patent exclusivity expires in 2028.

That sentence is the hinge of the whole analysis. JAKAFI is strong enough to fund the transition, but not strong enough to remove the need for one.

OPZELURA As The Second Commercial Leg

OPZELURA is the most important non-JAKAFI commercial product because it has two things investors usually want to see in a follow-on asset: real sales and a distinct market position. Net sales were $143 million in Q1 2026, up from $119 million a year earlier. International sales reached $36.7 million, helped by uptake in Canada and Italy.

The strategic value is especially clear in vitiligo. FDA's approval language is unusually useful here: OPZELURA was the first approved pharmacologic treatment aimed at repigmentation in vitiligo. In a disease where older options included steroids, calcineurin inhibitors, and phototherapy, a topical JAK cream with an approved repigmentation label has a stronger story than an undifferentiated dermatology launch.

But the accounting and reimbursement risk is real. Incyte has accrued $245.9 million for incremental rebates that would be owed if CMS treats OPZELURA as a Medicaid line extension of JAKAFI. The company says the issue affected OPZELURA gross-to-net deductions by about 8.4% in the March 2026 quarter. That is not cosmetic. It can directly lower net sales and margin.

There is also patent litigation around potential OPZELURA generic competition. Incyte says some cream and method-of-use patents extend into 2031 and 2040, but litigation makes the effective protection less clean than a simple patent-date table suggests.

GVHD And mutCALR

NIKTIMVO helps Incyte look less like a hematology company tied to one drug. FDA approved axatilimab-csfr for chronic GVHD after at least two prior systemic therapies in August 2024. In the 79 patients treated at the recommended dose, the overall response rate was 75%. That is a meaningful label in a specialist disease.

The key is that NIKTIMVO is not just another JAK inhibitor. It blocks CSF-1R, so it gives Incyte a different mechanism in the same broad GVHD franchise. If a physician knows JAKAFI and later considers NIKTIMVO in a different line of therapy, Incyte gains more relevance in the treatment journey.

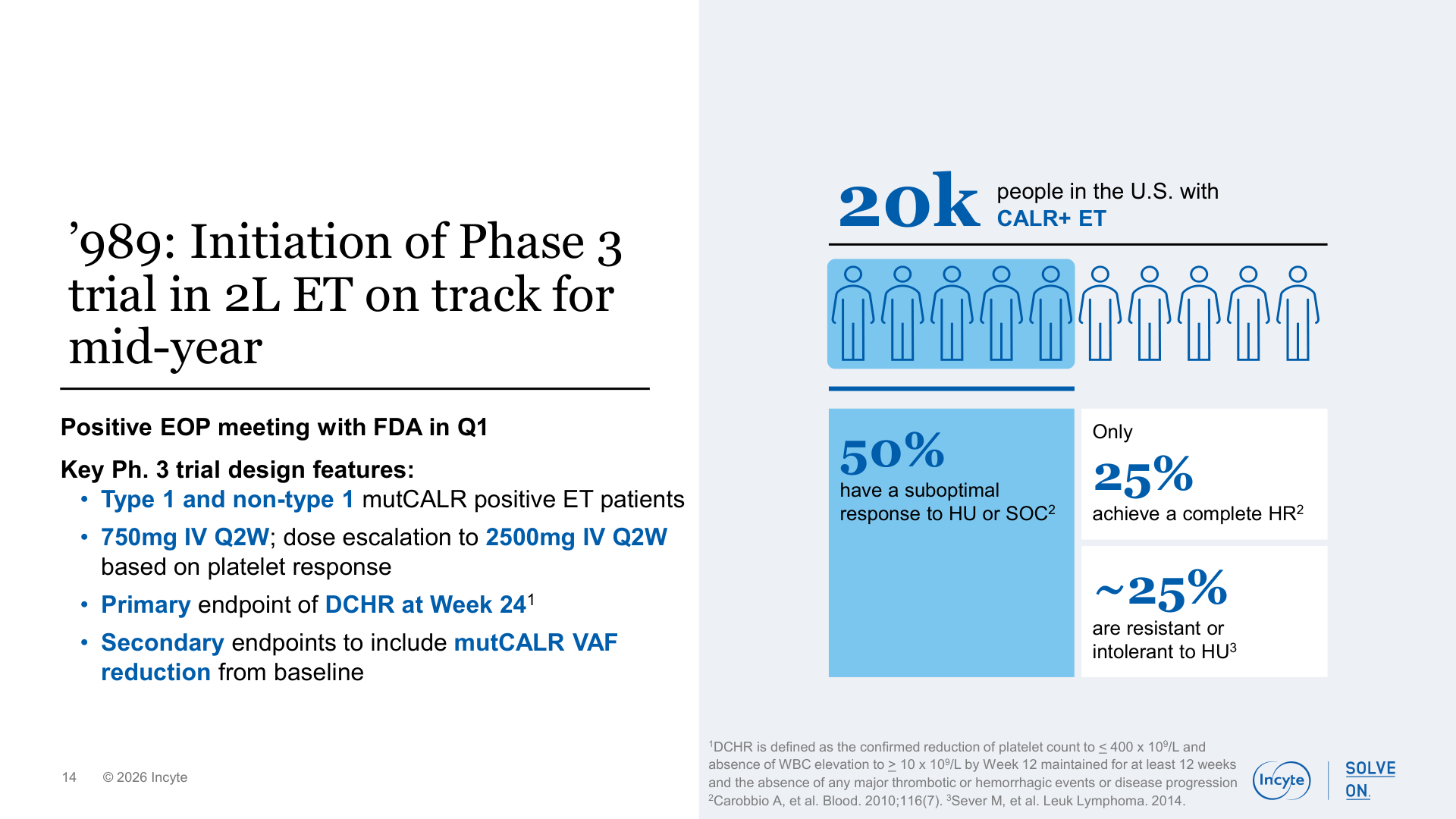

The larger long-term option is INCA033989, the mutCALR antibody. This is why Incyte should not be viewed only as a near-term patent-cliff story. The company says INCA033989 is designed to target mutant calreticulin in ET and myelofibrosis. A Phase 3 study in mutCALR-positive ET is planned to start in mid-2026, and a Phase 3 study in myelofibrosis is expected in the second half of 2026.

This is still a clinical option, not a proven advantage. But if a mutCALR therapy can show disease-modifying evidence, Incyte could build a new MPN franchise on top of the specialist network JAKAFI created. That is the most persuasive upside case.

| Asset | Evidence today | What would prove more |

|---|---|---|

| OPZELURA | Growing U.S. and international demand. | Cleaner gross-to-net conversion and litigation clarity. |

| NIKTIMVO | Fast launch from a small base in chronic GVHD. | Durable use beyond early uptake and stronger combination data. |

| ZYNYZ | Rising from a very small oncology base. | Growth that is not only a launch-year comparison effect. |

| mutCALR | Phase 3 starts are planned in 2026. | Clinical evidence that changes the MPN treatment frame. |

The Balance Sheet Gives Incyte Time

The financial picture gives Incyte room to attempt the transition. The company had $4.0 billion of cash, cash equivalents, and marketable securities at March 31, 2026. That matters because biotech transition stories often fail not only when clinical research disappoints, but when the company runs out of balance-sheet flexibility while waiting for data.

The income statement is also healthy. Q1 2026 net sales were $1.10 billion and total revenue was $1.27 billion. R&D expense was $516 million, up 18% year over year, but operating income still rose to $301 million. That suggests the company is not buying pipeline progress by destroying current profitability.

Cash flow confirms the quality. Operating cash flow was $369 million, while capital expenditures were only $10 million. Simple free cash flow was therefore about $359 million for the quarter. A drug company with low capex and high gross margins can fund a lot of late-stage work when the core product remains strong.

At roughly $99.85 per share on May 7, 2026, INCY sat near $20.6 billion of equity value and a P/E near 14.1x. That is not a valuation verdict. It simply suggests the market is giving Incyte credit for current cash generation while still discounting the post-JAKAFI uncertainty.

The balance sheet does not remove business risk. It simply makes the risk more about execution than survival.

What To Watch

The first item is JAKAFI demand before 2028. If JAKAFI begins fading earlier than expected, the preparation window narrows. If it holds, Incyte gets more time.

The second item is OPZELURA net sales quality. Gross sales are not enough. The market needs to watch gross-to-net deductions, CMS line-extension litigation, payer access, and generic litigation.

The third item is whether NIKTIMVO and ZYNYZ can keep growing after the easiest launch comparisons pass. Small bases can create exciting growth percentages; durable franchises require repeatable demand.

The fourth item is mutCALR Phase 3 execution. Patient enrollment, endpoint clarity, and early clinical signals will matter more than broad pipeline language.

The final item is cost discipline. R&D investment is necessary, but stock-based compensation, SG&A, and one-off capital allocation mistakes can dilute the quality of cash generation.

Bottom Line

Incyte is a financially strong company in a difficult transition. The current business is profitable, cash generative, and financially sturdy. The danger is not that Incyte lacks assets. The danger is that JAKAFI is still so large that every replacement asset must be judged against a high bar.

The fair conclusion is balanced: Incyte has a clear competitive advantage today, but the decisive question is whether that advantage can move beyond JAKAFI into a broader post-2028 franchise. OPZELURA and NIKTIMVO are the second commercial leg. mutCALR is the most interesting long-term option. Until those pieces prove more, the discount around JAKAFI patent-expiry risk is understandable.

Sources

- Incyte Form 10-Q for the quarter ended March 31, 2026

- Incyte Q1 2026 earnings release, April 28, 2026

- Incyte Q1 2026 Financial and Corporate Update Presentation, April 28, 2026

- Incyte FY2025 Form 10-K

- Jakafi.com dosage page

- OPZELURA HCP dosing page

- Incyte portfolio page

- Incyte, What Can JAK Inhibition Do? More Than You Might Think

- FDA, OPZELURA vitiligo approval summary

- FDA, NIKTIMVO chronic GVHD approval summary

- FDA, JAKAFI chronic GVHD approval summary